Tree-Based Methods

-

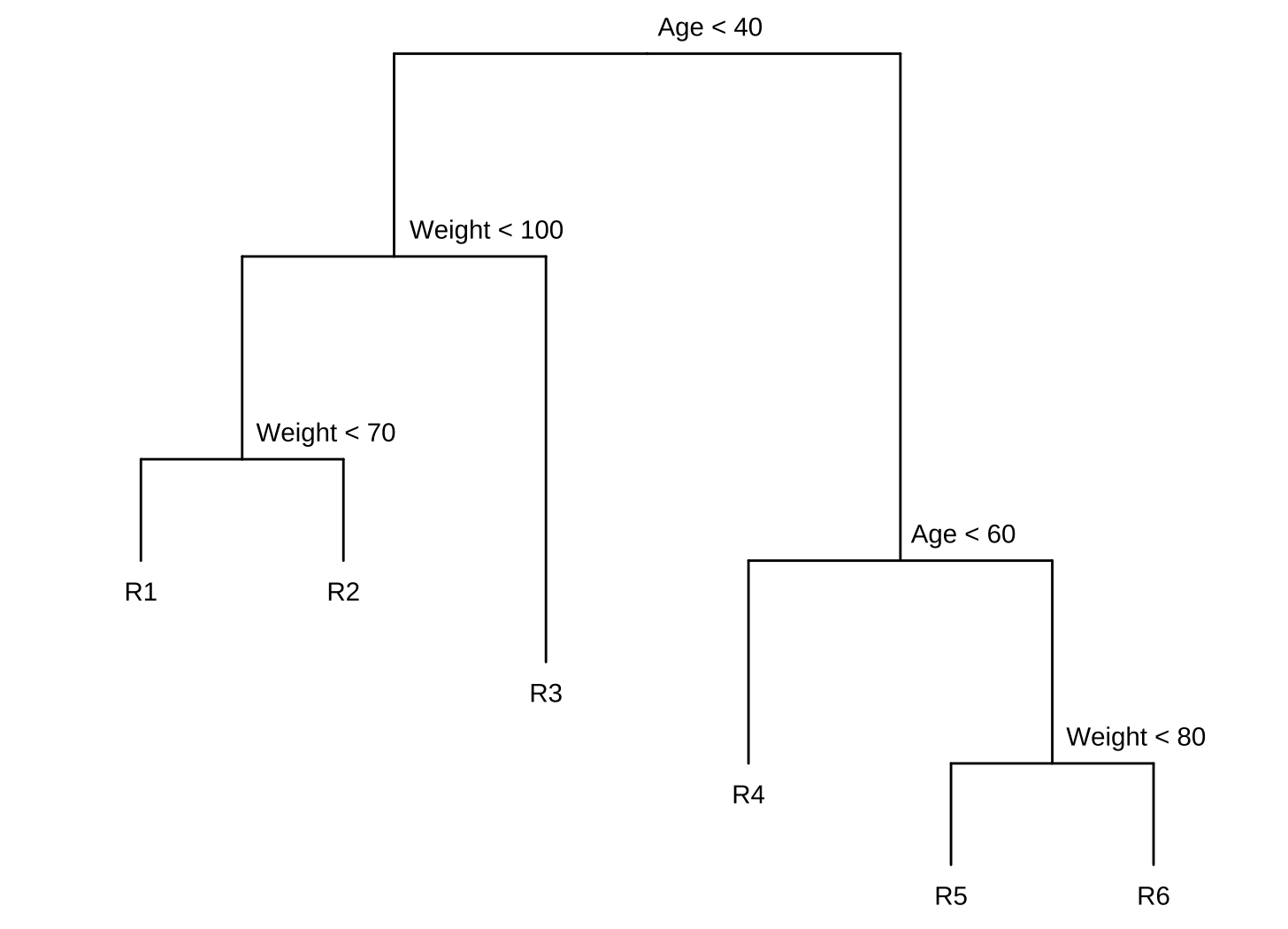

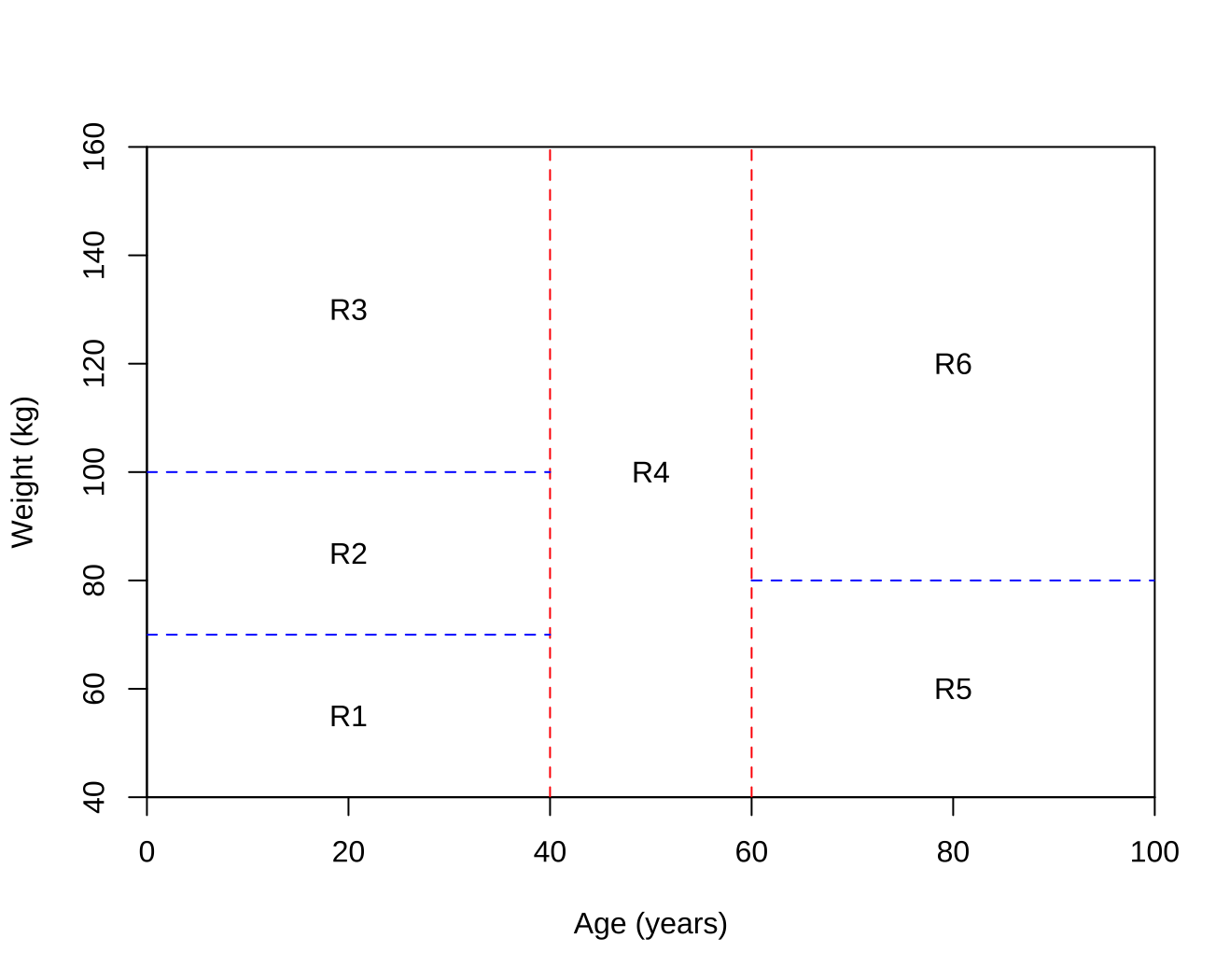

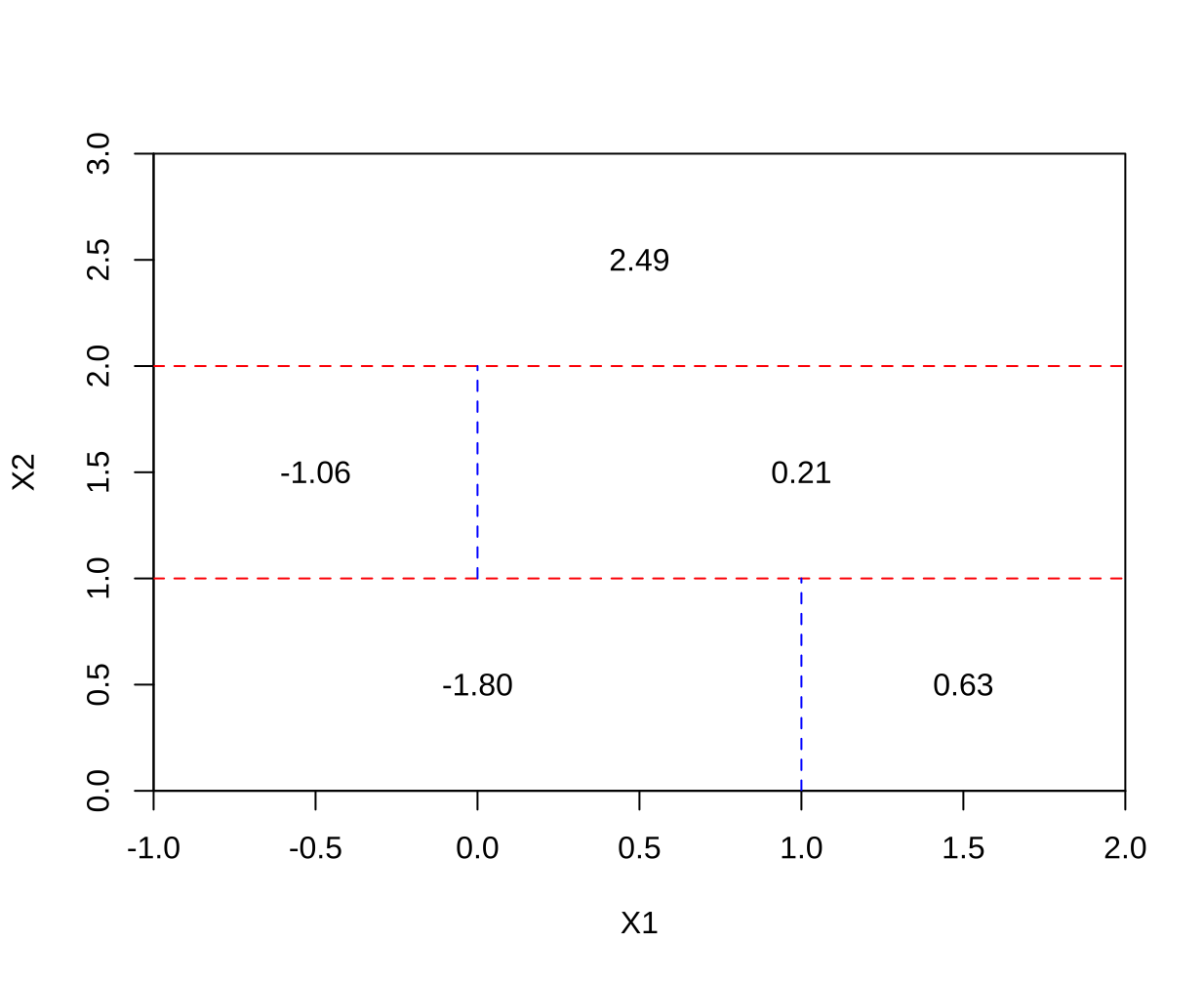

Draw an example (of your own invention) of a partition of two-dimensional feature space that could result from recursive binary splitting. Your example should contain at least six regions. Draw a decision tree corresponding to this partition. Be sure to label all aspects of your figures, including the regions $R_1$, $R_2$, . . ., the cutpoints $t_1$, $t_2$, . . ., and so forth.

Hint: Your result should look something like Figures 8.1. and 8.2.

-

It is mentioned in Section 8.2.3 that boosting using depth-one trees (or stumps) leads to an additive model: that is, a model of the form

\[f(X) = \sum\limits_{j=1}^p f_j (X_j).\]Explain why this is the case. You can begin with (8.12) in Algorithm 8.2.

Model addytywny ma postać $f(X) = \sum\limits_{j=1}^p f_j (X_j)$, gdzie ostateczna prognoza jest sumą funkcji, z których każda zależy tylko od jednego predyktora.

W przypadku boostingu z pniami (drzewami o głębokości 1), każde indywidualne drzewo $f^b(x)$ jest funkcją tylko jednej zmiennej (tej, która została użyta do podziału). Ostateczny model jest sumą wielu takich prostych drzew. Sumę tę można przegrupować tak, aby zsumować wszystkie funkcje zależne od $X_1$, wszystkie funkcje zależne od $X_2$ itd., co prowadzi bezpośrednio do addytywnej formy modelu.

-

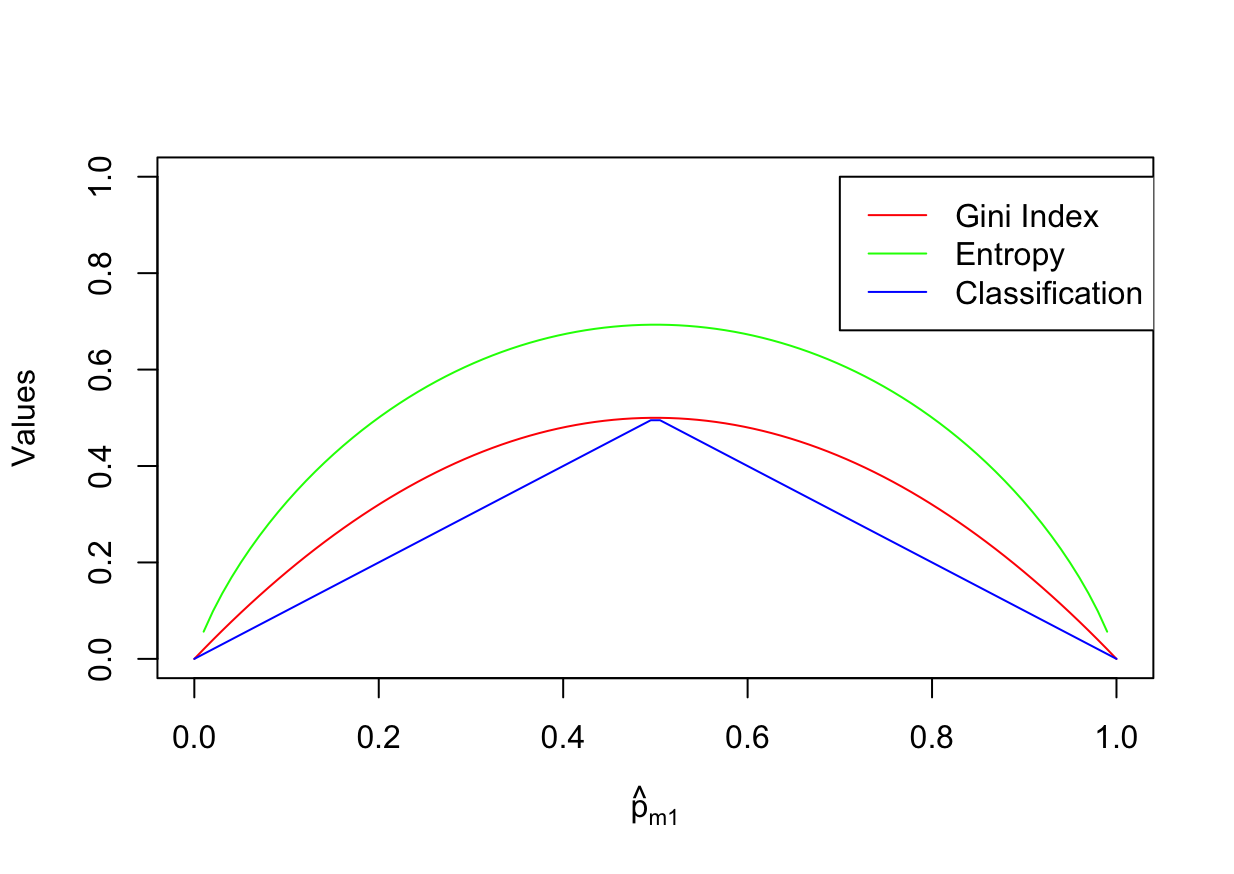

Consider the Gini index, classification error, and entropy in a simple classification setting with two classes. Create a single plot that displays each of these quantities as a function of $\hat{p}_{m1}$.

The $x$-axis should display $\hat{p}_{m1}$, ranging from 0 to 1, and the $y$-axis should display the value of the Gini index, classification error, and entropy.

Hint: In a setting with two classes, $\hat{p}{m1} = 1 - \hat{p}{m2}$ You could make this plot by hand, but it will be much easier to make in

R.Gini index:

\[G = \sum\limits_{k=1}^K \hat{p}_{mk} (1 - \hat{p}_{mk})\]Entropy:

\[D = -\sum\limits_{k=1}^K \hat{p}_{mk} \log\hat{p}_{mk}\]Classification error:

\[E = 1 - \sum\limits_{k=1}^K \max_k (\hat{p}_{mk})\]p <- seq(0, 1, length.out = 100) data <- data.frame( x = p, "G" = p * (1 - p) * 2, "D" = -(p * log(p) + (1 - p) * log(1 - p)), "E" = 1 - pmax(p, 1 - p), check.names = FALSE ) plot(data$x, data$G, type = "l", col = "red", xlab = expression(hat(p)[m1]), ylab = "Values", ylim=c(0, 1)) lines(data$x, data$D, type = "l", col = "green") lines(data$x, data$E, type = "l", col = "blue") legend(0.7,1,legend=c("Gini Index", "Entropy", "Classification Error"), col=c("red", "green", "blue"), lwd=c(1,1,1))

-

This question relates to the plots in Figure 8.14.

(a) Sketch the tree corresponding to the partition of the predictor space illustrated in the left-hand panel of Figure 8 14. The numbers inside the boxes indicate the mean of $Y$ within each region.

(b) Create a diagram similar to the left-hand panel of Figure 8.14, using the tree illustrated in the right-hand panel of the same figure. You should divide up the predictor space into the correct regions, and indicate the mean for each region.

-

Suppose we produce ten bootstrapped samples from a data set containing red and green classes. We then apply a classification tree to each bootstrapped sample and, for a specific value of $X$, produce 10 estimates of $P(\text{Class is Red} \mid X)$:

\[0.1, 0.15, 0.2, 0.2, 0.55, 0.6, 0.6, 0.65, 0.7, \text{ and } 0.75.\]There are two common ways to combine these results together into a single class prediction. One is the majority vote approach discussed in this chapter. The second approach is to classify based on the average probability. In this example, what is the final classification under each of these two approaches?

-

Majority vote:

Zliczenia $P(\text{Class is Red} \mid X) < 0.5 = 4$.

Zliczenia $P(\text{Class is Red} \mid X) \ge 0.5 = 6$.

Klasyfikacja jako

Red. -

Average probability:

$4.5 / 10 = 0.45$

Klasyfikacja jako

Green.

-

-

Provide a detailed explanation of the algorithm that is used to fit a regression tree.

I: Budowa drzewa za pomocą rekurencyjnego podziału binarnego

Celem tego kroku jest podzielenie przestrzeni predyktorów na zbiór odrębnych, niepokrywających się regionów o prostokątnym kształcie. Algorytm jest “odgórny” i “zachłanny” (top-down, greedy), co oznacza, że zaczyna od wszystkich danych w jednym regionie i na każdym kroku dokonuje najlepszego możliwego podziału.

1. Kryterium podziału:

Głównym celem jest znalezienie regionów $R_1, R_2, …, R_J$, które minimalizują sumę kwadratów reszt (RSS):

\[RSS = \sum_{j=1}^{J} \sum_{i \in R_j} (y_i - \hat{y}_{R_j})^2\]gdzie $\hat{y}_{R_j}$ to średnia wartość zmiennej odpowiedzi dla obserwacji treningowych w regionie $R_j$.

2. Proces podziału:

- Krok 1: Algorytm zaczyna z wszystkimi obserwacjami w jednym regionie.

- Krok 2: Następnie rozważa wszystkie predyktory $X_1, X_2, …, X_p$ i wszystkie możliwe punkty cięcia $s$ dla każdego z predyktorów. Wybierany jest ten predyktor $X_j$ i ten punkt cięcia $s$, które dzielą przestrzeń na dwa nowe regiony (${X\mid X_j < s}$ i ${X\mid X_j \ge s}$) tak, aby uzyskać największą możliwą redukcję RSS.

- Krok 3: Proces jest powtarzany dla każdego z nowo utworzonych regionów.

- Krok 4: Działania te kontynuuje się do momentu spełnienia kryterium stopu, na przykład, gdy każdy region końcowy (liść) zawiera mniej niż pewną minimalną liczbę obserwacji.

W wyniku tego procesu powstaje duże, często przetrenowane (overfitted) drzewo, które dobrze radzi sobie z danymi treningowymi, ale prawdopodobnie słabo z danymi testowymi.

II: Przycinanie drzewa (pruning)

Aby uniknąć nadmiernego dopasowania, duże drzewo uzyskane w punkcie I jest przycinane w celu znalezienia mniejszego poddrzewa, które ma niższy błąd na danych testowych.

1. Metoda: przycinanie według złożoności kosztu (cost complexity pruning)

Zamiast rozważać każde możliwe poddrzewo, metoda ta generuje sekwencję poddrzew w funkcji nieujemnego parametru dostrajania $\alpha$. Dla każdej wartości $\alpha$ znajduje się poddrzewo $T$, które minimalizuje następujące wyrażenie:

\[\sum_{m=1}^{\mid T \mid} \sum_{i: x_i \in R_m} (y_i - \hat{y}_{R_m})^2 + \alpha\mid T \mid\]- Pierwszy człon to suma kwadratów reszt (RSS), która mierzy dopasowanie do danych treningowych.

- Drugi człon, $\alpha\mid T \mid$, to kara za złożoność, gdzie $\mid T \mid$ jest liczbą liści (węzłów końcowych) w drzewie.

- Parametr $\alpha$ kontroluje kompromis między dopasowaniem a złożonością. Gdy $\alpha = 0$, otrzymujemy oryginalne, duże drzewo. W miarę wzrostu $\alpha$, preferowane są mniejsze poddrzewa.

2. Wybór optymalnego parametru $\alpha$:

Optymalna wartość parametru $\alpha$ jest wybierana za pomocą K-krotnej walidacji krzyżowej (K-fold cross-validation). Dla różnych wartości $\alpha$ obliczany jest średni błąd na zbiorach walidacyjnych, a następnie wybierane jest to $\alpha$, które minimalizuje ten błąd.

-

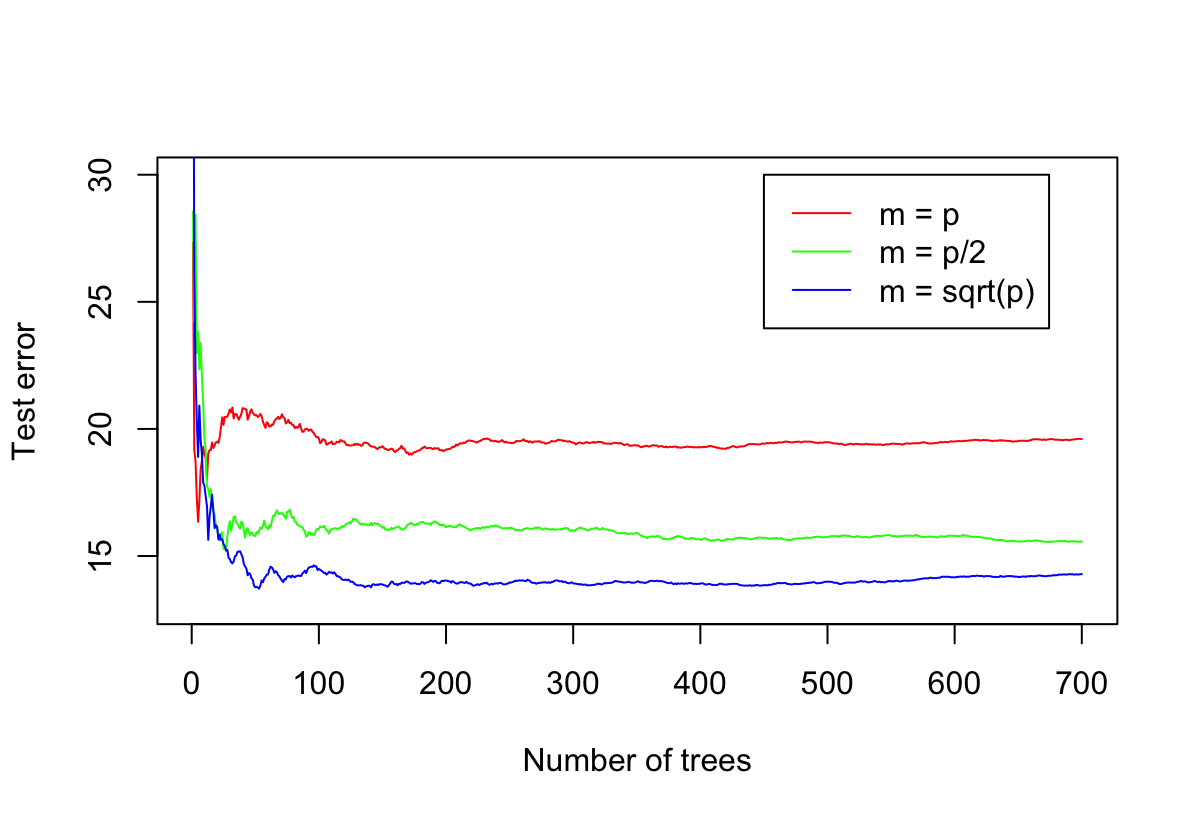

In the lab, we applied random forests to the

Bostondata usingmtry = 6and usingntree = 25andntree = 500. Create a plot displaying the test error resulting from random forests on this data set for a more comprehensive range of values formtryandntree. You can model your plot after Figure 8.10. Describe the results obtained.library(ISLR2) library(randomForest) attach(Boston) set.seed(1) train <- sample(nrow(Boston), nrow(Boston) * 2 / 3) p = 12 n = 700 fit_1 <- randomForest(x = Boston[train, -13], y = Boston[train, 13], xtest = Boston[-train, -13], ytest = Boston[-train, 13], mtry = p, ntree = n) fit_2 <- randomForest(x = Boston[train, -13], y = Boston[train, 13], xtest = Boston[-train, -13], ytest = Boston[-train, 13], mtry = p / 2, ntree = n) fit_3 <- randomForest(x = Boston[train, -13], y = Boston[train, 13], xtest = Boston[-train, -13], ytest = Boston[-train, 13], mtry = sqrt(p), ntree = n) plot(1:n, fit_1$test$mse, type = "l", ylim = c(13, 30), col = "red", xlab = "Number of trees", ylab = "Test error") lines(1:n, fit_2$test$mse, type = "l", col = "green") lines(1:n, fit_3$test$mse, type = "l", col = "blue") legend(450, 30, legend=c("m = p", "m = p/2", "m = sqrt(p)"), col=c("red", "green", "blue"), lwd=c(1,1,1))

Błąd dąży do pewnej w miarę stabilnej wartości wraz ze wzrostem liczby drzew.

Błąd jest mniejszy jeżeli zmniejszymy $m$.

-

In the lab, a classification tree was applied to the

Carseatsdata set after convertingSalesinto a qualitative response variable. Now we will seek to predictSalesusing regression trees and related approaches, treating the response as a quantitative variable.(a) Split the data set into a training set and a test set.

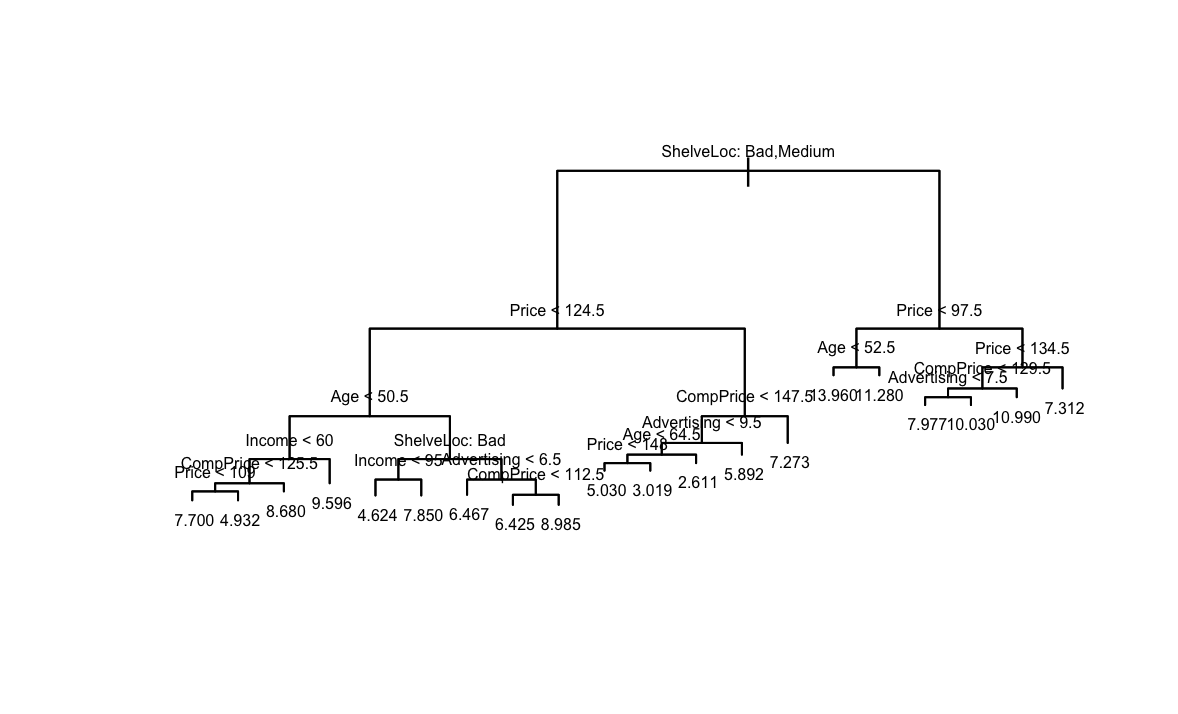

library(ISLR2) library(randomForest) library(tree) attach(Carseats) set.seed(42) train <- sample(nrow(Carseats), nrow(Carseats) * 2 / 3)(b) Fit a regression tree to the training set. Plot the tree, and interpret the results. What test MSE do you obtain?

fit <- tree(Sales ~ ., data = Carseats[train, ]) plot(fit) text(fit, pretty = 0, cex = 0.5) yhat <- predict(fit, newdata = Carseats[-train, ]) test <- Carseats[-train, "Sales"] mean((yhat - test)^2)[1] 4.945247

Najważniejsze zmienne to

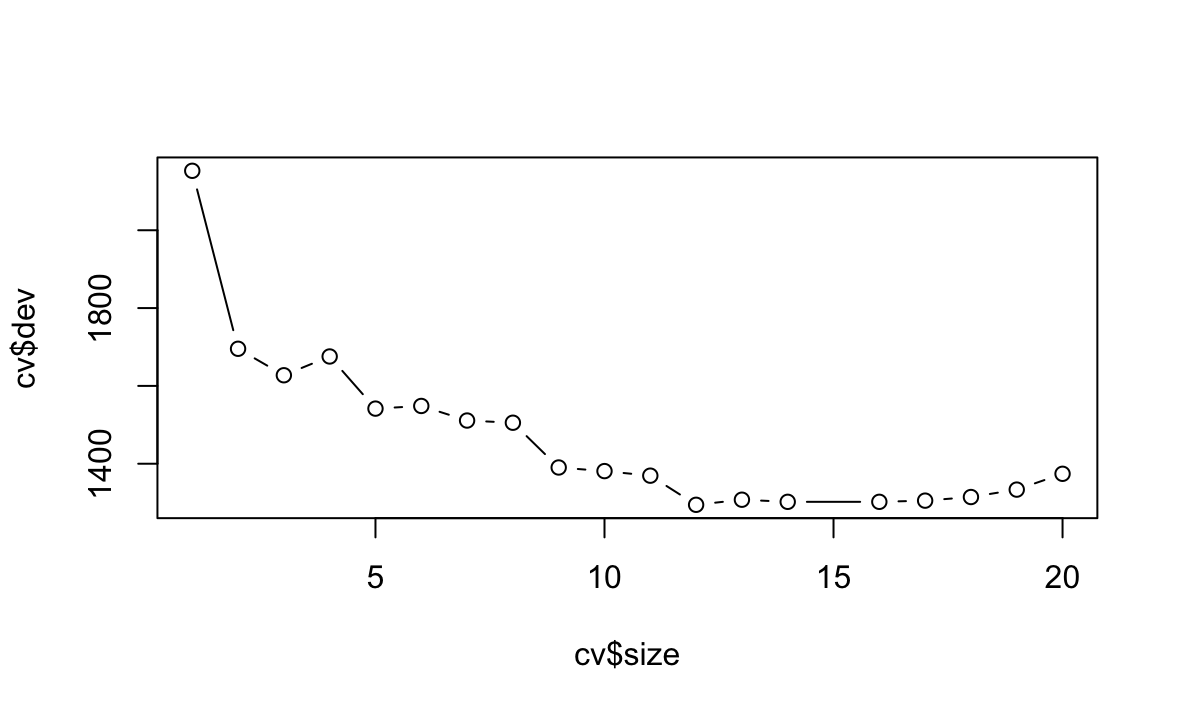

ShelveLociPrice.(c) Use cross-validation in order to determine the optimal level of tree complexity. Does pruning the tree improve the test MSE?

cv <- cv.tree(fit) plot(cv$size, cv$dev, type = "b") prune <- prune.tree(fit, best = 4) yhat <- predict(prune, newdata = Carseats[-train, ]) test <- Carseats[-train, "Sales"] mean((yhat - test)^2)[1] 4.476256

Z wykresu widać, że należy przyciąć drzewo do rozmiaru 12, nieznacznie polepsza to MSE.

(d) Use the bagging approach in order to analyze this data. What test MSE do you obtain? Use the

importance()function to determine which variables are most important.bag.fit = randomForest(Sales ~ ., data = Carseats[train, ], mtry = 10, importance = T) importance(bag.fit)%IncMSE IncNodePurity CompPrice 34.442203 275.877646 Income 10.594604 118.555454 Advertising 21.112431 166.883279 Population 1.691055 84.322807 Price 67.336617 616.752513 ShelveLoc 72.275993 574.237721 Age 17.055485 178.235283 Education 4.934414 56.817835 Urban 2.294690 9.594651 US 2.908003 8.278551yhat <- predict(bag.fit, newdata = Carseats[-train, ]) test <- Carseats[-train, "Sales"] mean((yhat - test)^2)[1] 2.098377Najważniejsza jest zmienna

Price. Bagging poprawił też poziom błędu MSE.(e) Use random forests to analyze this data. What test MSE do you obtain? Use the

importance()function to determine which variables are most important. Describe the effect of $m$, the number of variables considered at each split, on the error rate obtained.bag.fit = randomForest(Sales ~ ., data = Carseats[train, ], mtry = 3, importance = T) importance(bag.fit)%IncMSE IncNodePurity CompPrice 16.389686 206.08152 Income 5.675147 163.24324 Advertising 16.345509 208.15730 Population 2.711832 137.71273 Price 43.225770 467.82974 ShelveLoc 47.486572 459.10402 Age 13.857215 214.79994 Education 1.932250 102.18150 Urban 2.561229 20.06366 US 3.667538 30.08216yhat <- predict(bag.fit, newdata = Carseats[-train, ]) test <- Carseats[-train, "Sales"] mean((yhat - test)^2)[1] 2.741097Najważniejsza jest zmienna

Price. Zmiana parametru $m$ pogarsza wartość błędu MSE.(f) Now analyze the data using BART, and report your results.

bart.fit <- gbart(Carseats[train, 2:11], Carseats[train, 1], x.test = Carseats[-train, 2:11]) yhat <- bart.fit$yhat.test.mean test <- Carseats[-train, 1] mean((test - yhat)^2)[1] 1.360843Model BART pozwolił jeszcze bardziej zmniejszyć błąd MSE.

-

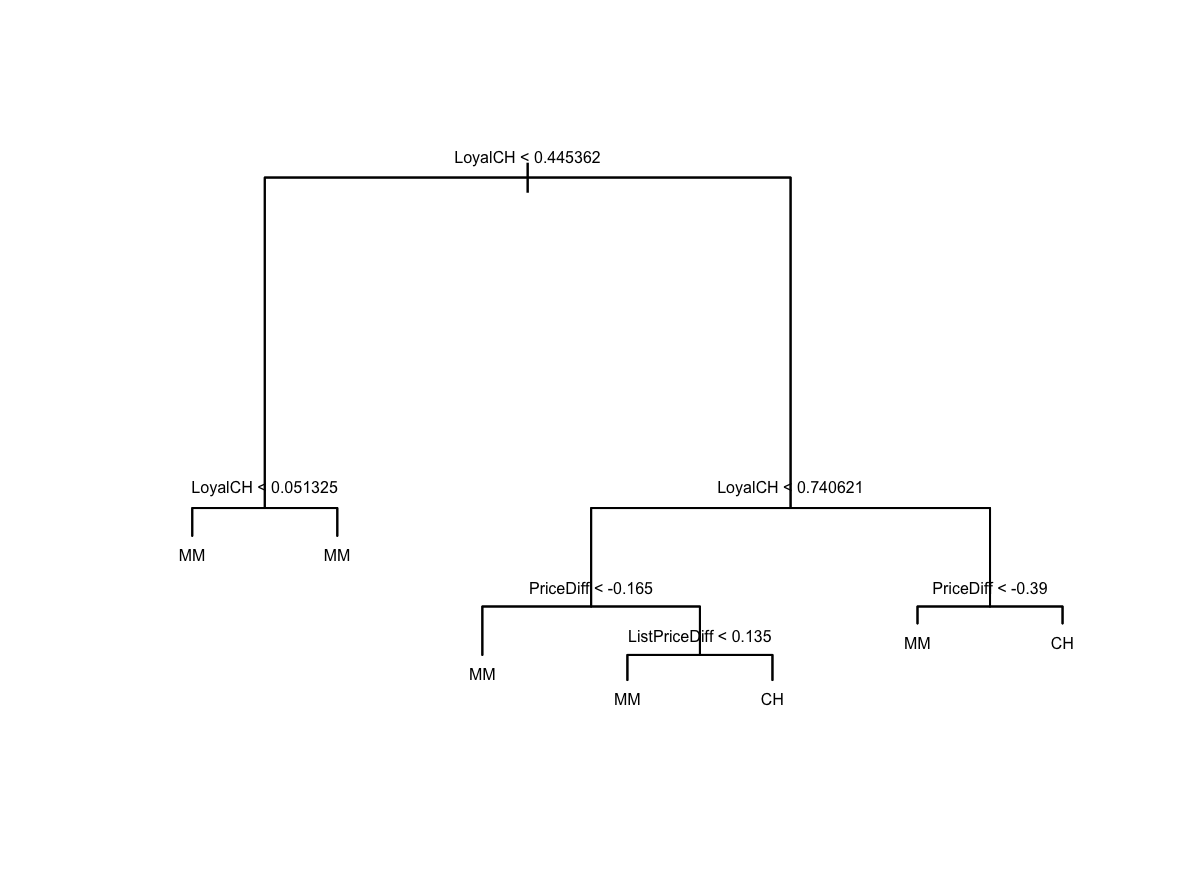

This problem involves the

OJdata set which is part of theISLR2package.(a) Create a training set containing a random sample of 800 observations, and a test set containing the remaining observations.

library(ISLR2) library(randomForest) library(tree) library(BART) attach(OJ) set.seed(42) train <- sample(nrow(OJ), 800)(b) Fit a tree to the training data, with

Purchaseas the response and the other variables as predictors. Use thesummary()function to produce summary statistics about the tree, and describe the results obtained. What is the training error rate? How many terminal nodes does the tree have?fit <- tree(Purchase ~ ., data = OJ[train, ]) summary(fit)Classification tree: tree(formula = Purchase ~ ., data = OJ[train, ]) Variables actually used in tree construction: [1] "LoyalCH" "PriceDiff" "ListPriceDiff" Number of terminal nodes: 7 Residual mean deviance: 0.7598 = 602.5 / 793 Misclassification error rate: 0.155 = 124 / 800Błąd treningowy wynosi 0.155. Drzewo ma 7 węzłów końcowych. Dewiancja jest wysoka więc model nie jest dobry jakościowo.

(c) Type in the name of the tree object in order to get a detailed text output. Pick one of the terminal nodes, and interpret the information displayed.

fitnode), split, n, deviance, yval, (yprob) * denotes terminal node 1) root 800 1081.00 CH ( 0.59250 0.40750 ) 2) LoyalCH < 0.445362 279 277.00 MM ( 0.19713 0.80287 ) 4) LoyalCH < 0.051325 64 10.30 MM ( 0.01562 0.98438 ) * 5) LoyalCH > 0.051325 215 242.40 MM ( 0.25116 0.74884 ) * 3) LoyalCH > 0.445362 521 515.30 CH ( 0.80422 0.19578 ) 6) LoyalCH < 0.740621 249 324.70 CH ( 0.64257 0.35743 ) 12) PriceDiff < -0.165 39 36.71 MM ( 0.17949 0.82051 ) * 13) PriceDiff > -0.165 210 245.60 CH ( 0.72857 0.27143 ) 26) ListPriceDiff < 0.135 34 45.23 MM ( 0.38235 0.61765 ) * 27) ListPriceDiff > 0.135 176 178.30 CH ( 0.79545 0.20455 ) * 7) LoyalCH > 0.740621 272 104.40 CH ( 0.95221 0.04779 ) 14) PriceDiff < -0.39 8 11.09 MM ( 0.50000 0.50000 ) * 15) PriceDiff > -0.39 264 78.51 CH ( 0.96591 0.03409 ) *Węzeł nr 15 jest jednym z węzłów ostatnich, jest w nim 264 obserwacje. Jeżeli

LPriceDiff > -0.39to ostateczna wartość w tym węźle jest klasyfikowana jakoCH.(d) Create a plot of the tree, and interpret the results.

Najważniejsza jest zmienna

LoyalCH.(e) Predict the response on the test data, and produce a confusion matrix comparing the test labels to the predicted test labels. What is the test error rate?

pred <- predict(fit, OJ[-train, ], type = "class") t <- table(pred, OJ[-train, ]$Purchase) 1 - sum(diag(t)) / sum(t)[1] 0.2222222Błąd jest większy niż na danych treningowych czyli zgodnie z oczekiwaniem

(f) Apply the

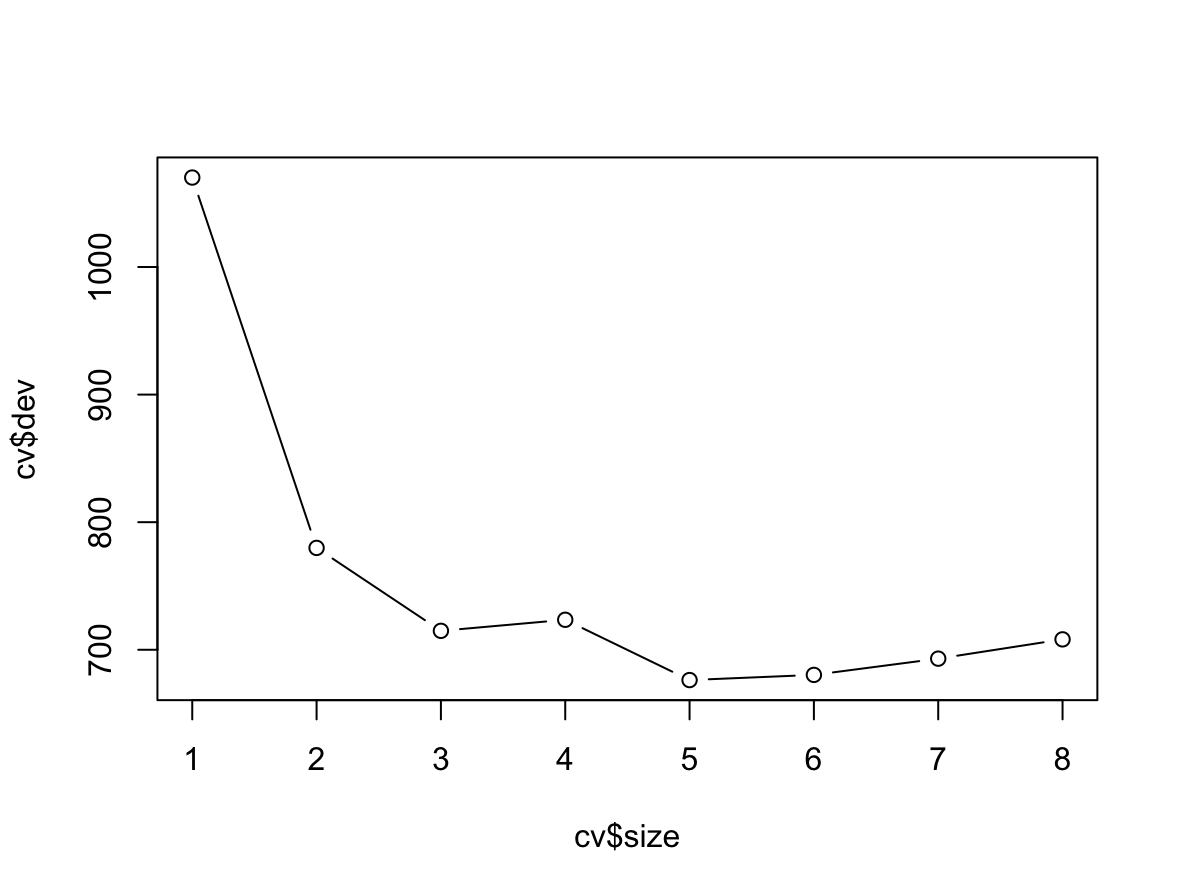

cv.tree()function to the training set in order to determine the optimal tree size.cv <- cv.tree(fit)(g) Produce a plot with tree size on the $x$-axis and cross-validated classification error rate on the $y$-axis.

plot(cv$size, cv$dev, type = "b")

(h) Which tree size corresponds to the lowest cross-validated classification error rate?

Najmniejszy błąd jest dla drzewa o rozmiarze 5.

(i) Produce a pruned tree corresponding to the optimal tree size obtained using cross-validation. If cross-validation does not lead to selection of a pruned tree, then create a pruned tree with five terminal nodes.

prune <- prune.tree(fit, best = 5)(j) Compare the training error rates between the pruned and unpruned trees. Which is higher?

summary(prune)Classification tree: snip.tree(tree = fit, nodes = c(5L, 12L)) Variables actually used in tree construction: [1] "LoyalCH" "PriceDiff" Number of terminal nodes: 5 Residual mean deviance: 0.7833 = 622.7 / 795 Misclassification error rate: 0.1812 = 145 / 800Błąd 0.1812 jest wyższy niż na danych nie przyciętych.

(k) Compare the test error rates between the pruned and unpruned trees. Which is higher?

pred <- predict(prune, OJ[-train, ], type = "class") t <- table(pred, OJ[-train, ]$Purchase) 1 - sum(diag(t)) / sum(t)[1] 0.2185185Błąd na danych testowy jest nieznacznie niższy niż w przypadku modelu nie przyciętego.

-

We now use boosting to predict

Salaryin theHittersdata set.(a) Remove the observations for whom the salary information is unknown, and then log-transform the salaries.

library(ISLR2) Hitters_2 <- Hitters Hitters_2 <- Hitters_2[!is.na(Hitters_2$Salary), ] Hitters_2$Salary <- log(Hitters_2$Salary) attach(Hitters_2)(b) Create a training set consisting of the first 200 observations, and a test set consisting of the remaining observations.

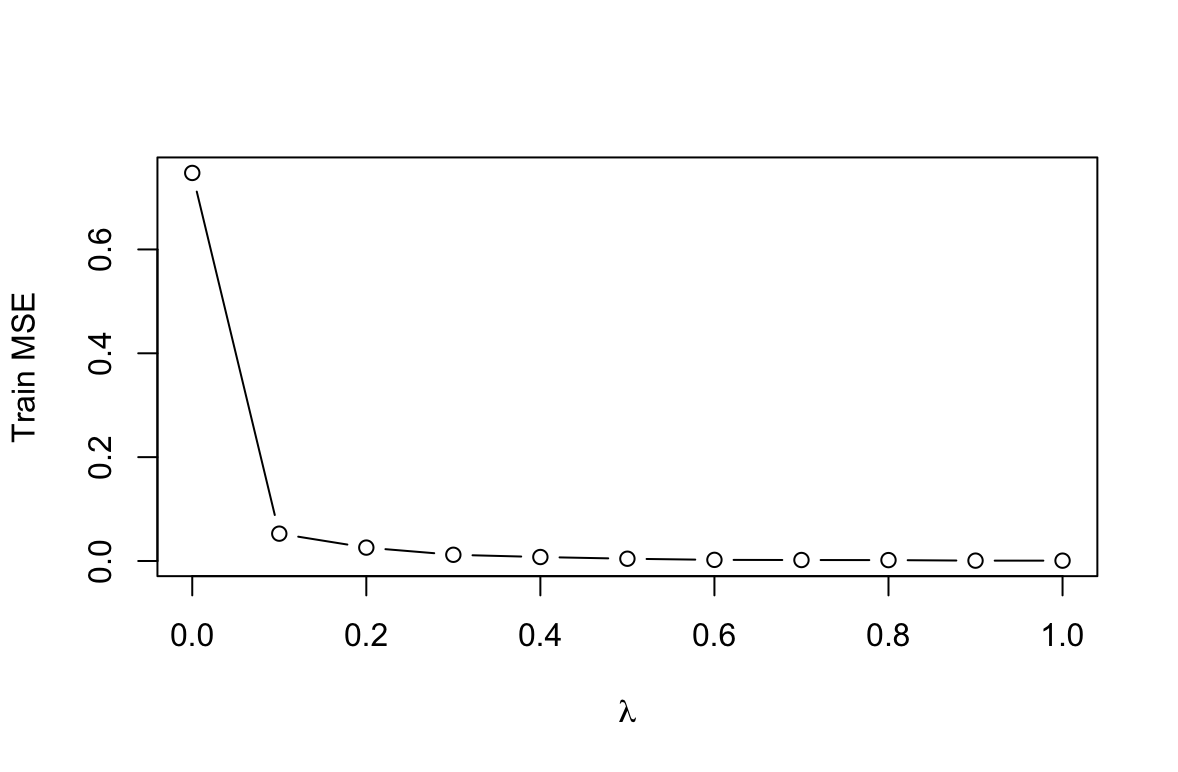

set.seed(2) train <- sample(nrow(Hitters_2), 200)(c) Perform boosting on the training set with 1,000 trees for a range of values of the shrinkage parameter $\lambda$. Produce a plot with different shrinkage values on the $x$-axis and the corresponding training set MSE on the $y$-axis.

library(gbm) lambdas <- seq(0, 1, 0.1) means <- c() for (i in lambdas){ boost <- gbm(Salary ~ ., data = Hitters_2[train, ], distribution = "gaussian", n.trees = 1000, shrinkage = i) yhat <- predict(boost, newdata = Hitters_2[train, ], n.trees = 1000) means <- c(means, mean((yhat - Hitters_2[train, ]$Salary)^2)) } plot(lambdas, means, type="b", xlab = expression(lambda), ylab = "Train MSE")

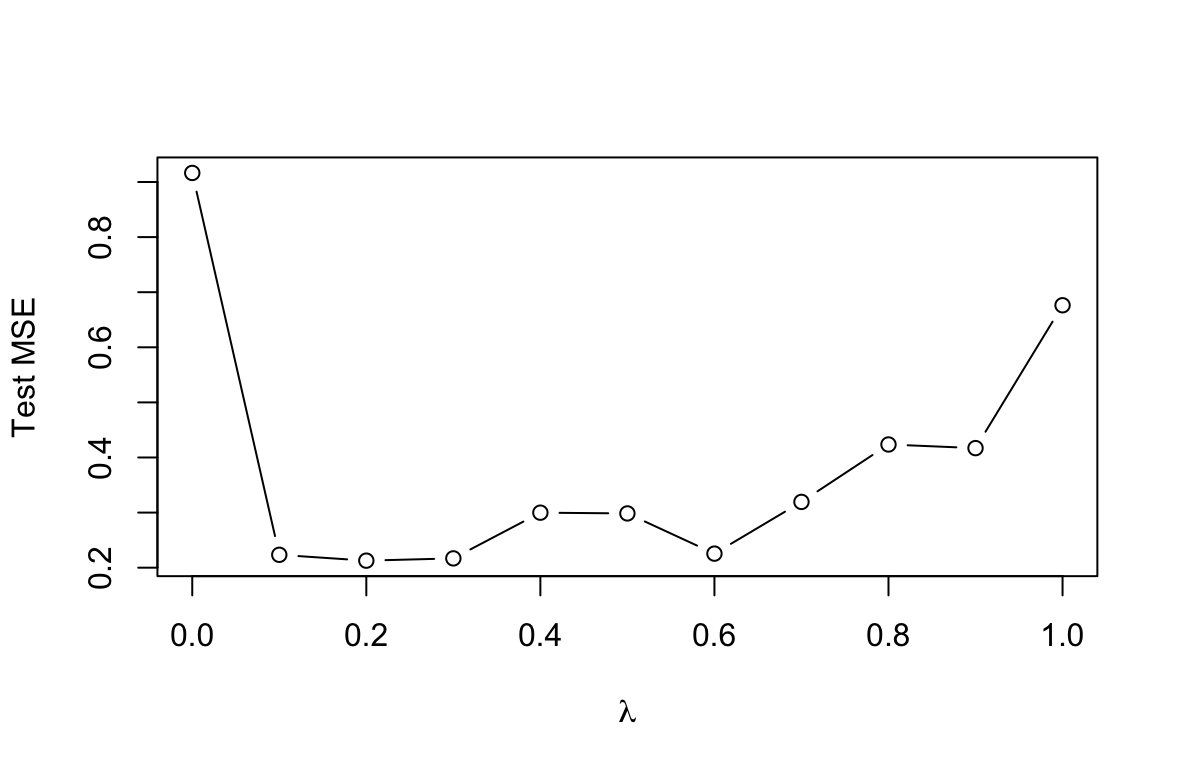

(d) Produce a plot with different shrinkage values on the $x$-axis and the corresponding test set MSE on the $y$-axis.

lambdas <- seq(0, 1, 0.1) means <- c() for (i in lambdas){ boost <- gbm(Salary ~ ., data = Hitters_2[train, ], distribution = "gaussian", n.trees = 1000, shrinkage = i) yhat <- predict(boost, newdata = Hitters_2[-train, ], n.trees = 1000) means <- c(means, mean((yhat - Hitters_2[-train, ]$Salary)^2)) } min(means) lambdas[which.min(means)] plot(lambdas, means, type="b", xlab=expression(lambda), ylab="Test MSE")[1] 0.2127571 [1] 0.2

(e) Compare the test MSE of boosting to the test MSE that results from applying two of the regression approaches seen in Chapters 3 and 6.

# Multiple Linear Regression (Chapter 3) lm.fit = lm(Salary ~ ., data = Hitters_2[train, ]) lm.preds = predict(lm.fit, newdata = Hitters_2[-train, ]) lm.mse = mean((lm.preds - Hitters_2[-train, ]$Salary)^2) lm.mse[1] 0.5143062# Lasso model (Chapter 6) library(glmnet) x = model.matrix(Salary ~ ., data = Hitters_2[train, ]) test = model.matrix(Salary ~ ., data = Hitters_2[-train, ]) y = Hitters_2[train, ]$Salary lasso.mod = glmnet(x, y, alpha = 1) cv.out = cv.glmnet(x, y, alpha=1) bestlam = cv.out$lambda.min lasso.pred = predict(lasso.mod, s=bestlam, newx = test) mean((lasso.pred - Hitters_2[-train, ]$Salary)^2)[1] 0.4742347Drzewo zbudowane metodą boosting ma w tym przypadku mniejszy błąd niż regresja liniowa i lasso.

(f) Which variables appear to be the most important predictors in the boosted model?

boost = gbm(Salary ~ ., data= Hitters_2[train, ], distribution = "gaussian", n.trees = 1000, shrinkage = 0.2) summary(boost)var rel.inf CWalks CWalks 11.5228111 CRuns CRuns 9.2845927 CRBI CRBI 9.1029165 PutOuts PutOuts 7.2472499 CHits CHits 6.6068264 HmRun HmRun 5.8016634 Walks Walks 5.7280674 AtBat AtBat 5.6755620 Hits Hits 5.6323046 Assists Assists 5.4405301 CAtBat CAtBat 4.9387237 Years Years 4.8418310 CHmRun CHmRun 4.7014300 Runs Runs 4.5384478 RBI RBI 4.5292375 Errors Errors 2.6463223 Division Division 0.8631037 NewLeague NewLeague 0.5374887 League League 0.3608911Najważniejsze zmienne w tym modelu to:

CWalks,CRuns,CRBI.(g) Now apply bagging to the training set. What is the test set MSE for this approach?

library(randomForest) bag = randomForest(Salary ~ ., data = Hitters_2[train, ], mtry = 19, importance = T) pred = predict(bag, newdata = Hitters_2[-train, ]) mean((pred - Hitters_2[-train, ]$Salary)^2)[1] 0.1913495Błąd mniejszy niż w przypadku boostingu.

-

This question uses the

Caravandata set.(a) Create a training set consisting of the first 1,000 observations, and a test set consisting of the remaining observations.

library(ISLR2) library(gbm) # funkcja gbm nie przyjmuje zmiennych w postaci no/yes Caravan_2 <- Caravan Caravan_2$Purchase_2 <- as.numeric(Caravan$Purchase == "Yes") train.set <- Caravan_2[1:1000, ] test.set <- Caravan_2[1001:5822, ](b) Fit a boosting model to the training set with

Purchaseas the response and the other variables as predictors. Use 1,000 trees, and a shrinkage value of 0.01. Which predictors appear to be the most important?set.seed(5) fit <- gbm(Purchase_2 ~ . - Purchase, data = train.set, n.trees = 1000, shrinkage = 0.01) head(summary(fit))var rel.inf PPERSAUT PPERSAUT 14.635194 MKOOPKLA MKOOPKLA 10.807759 MOPLHOOG MOPLHOOG 6.462813 MBERMIDD MBERMIDD 6.361418 PBRAND PBRAND 5.348285 MGODGE MGODGE 4.148591(c) Use the boosting model to predict the response on the test data. Predict that a person will make a purchase if the estimated probability of purchase is greater than 20%. Form a confusion matrix. What fraction of the people predicted to make a purchase do in fact make one? How does this compare with the results obtained from applying KNN or logistic regression to this data set?

p <- predict(fit, test.set, n.trees = 1000, type = "response") preds <- rep("No", 4822) preds[p > 0.20] = "Yes" actual <- test.set$Purchase table(actual, preds) 35 / (123+35)preds actual No Yes No 4410 123 Yes 254 35 [1] 0.221519# logistic regression train.set <- Caravan[1:1000, ] test.set <- Caravan[1001:5822, ] fit <- glm(Purchase ~ ., data = train.set, family = "binomial") p <- predict(fit, test.set, type = "response") preds <- rep("No", 4822) preds[p > 0.20] = "Yes" actual <- test.set$Purchase table(actual, preds) 58 / (350 + 58)preds actual No Yes No 4183 350 Yes 231 58 [1] 0.1421569# KNN library(class) fit <- knn(train.set[, -86], test.set[, -86], train.set$Purchase) table(actual, fit) 23 / (273 + 23)fit actual No Yes No 4260 273 Yes 266 23 [1] 0.0777027Ostatecznie boosting model najlepiej przewiduje odpowiedź

Yesze wszystkich dopasowanych modeli. -

Apply boosting, bagging, random forests, and BART to a data set of your choice. Be sure to fit the models on a training set and to evaluate their performance on a test set. How accurate are the results compared to simple methods like linear or logistic regression? Which of these approaches yields the best performance?